In the consumer world, companies know how important it is to understand their customers’ diverse needs. Only by doing this can they tailor products and services based on demographic, behaviour and habit in order to maximise value.

In the modern workplace, it stands to reason that employers can benefit from doing something similar: understanding workers well enough to know what motivates them at various stages of the employment life cycle. The execution does not need to be sophisticated. Fundamentally, this is about an organisation ensuring that its reward and benefits strategy is not only fit-for-purpose and agile but is also valued by its employees.

The modern reality is that workers no longer stay with a single employer for life. These days, an employee might start as an apprentice or graduate, work and achieve well enough to gain progression and promotions before moving towards retirement. This seems simple enough but when you overlay the same worker’s personal life and financial implications, things get a lot more complicated. There is saving for a first car or family holidays; then affording ‘big’ life events such as buying a house or getting married; then having children means a different kind of commitment in terms of time and money, often right through to retirement age. Seen through this lens, it is imperative that a benefits strategy is not only product-led but also combines a holistic approach to benefits and wellbeing.

Demographics Analytics

In pure data terms we need to break employees down into groups: by gender, ethnicity, age, tenure, level, family status. Limiting this to five or six broad segments makes things manageable and the categories (described below) are not scientific but have been guided by ONS data to illustrate the different segments.

By combining this data with broader analysis of staff turnover, tenure, employee satisfaction and performance, we can start to understand why retention is more challenging for certain age ranges, and we can highlight common misalignments between the expectation and reality of an Employee Value Proposition.

Employee feedback

This data analysis is always a big step forward, but it will only ever take you so far. To understand motivations and expectations beyond broad groupings and eliminate assumptions - particularly around benefits - you need to get out there and talk with employees. Focus groups are great for gaining a deeper understanding of how to match affordability with value to employees, and by the end of this process, HR departments might look to produce a report not dissimilar to this.

Developing (age: up to 24)

- Starting to understand basic finances, living for the here and now

- Short-term planning and less employer loyalty

- Prioritises ability to buy holidays and take shorter breaks more often

- Choice and the ability to personalise the package is important

Forming (age: 25 to 34)

- Want to put finances to more use

- Need sufficient understanding in order to maximise financial support, eg around ISAs, big ticket purchases (house, car) and saving for wedding

- Buying and Selling holidays to provide flexibility of holidays over cash.

- Need to know what is available, and how they can do it.

- Responsibility and unique work experiences are important

- This group will weigh up decisions for job mobility and will go for more opportunities to progress in salary and career

Flourishing (age: 35 - 44)

- Finances are committed

- Every penny counts so need to understand any support and advice available to them for mortgages, car finance, childcare, and school fees.

- Work-life balance and professional interests are important

- Job security is important, as well as the opportunity to develop careers and earn a higher salary

- Decisions are likely to be balanced and carefully considered

Establishing (age: 45 - 54)

- More disposable cash with the ability to support children still living at home, with house deposits or attending higher education

- Health and long-term finances are becoming more important. Likely to start increasing pension contributions and making a will or achieving strong financial planning is a focus

- Personal interests are important and careers are well established, so something must impact or change significantly to contemplate leaving or making a sideways move

Mentoring (age: 55 - 59)

- This group has established job security and contentment if they feel their role has a purpose and is valued

- Company loyalty and a sense of duty and culture are key motivators

- With more disposable cash, health protection and retirement are now key priorities. Allied to this, there is a risk they may leave early once pension draw-down kicks in

- Require more advanced financial support to ensure their finances and investments are working for them and any assumptions are not wide of the mark

- Likely to look for opportunities in flexible working or around additional holiday entitlement

- Can and will make choices for health and happiness

Coaching (age: 60+)

- Likely to make increased contributions to pension and additional purchases for health cover

- Often putting in place legal frameworks such as Power of Attorney

- Nearing retirement so unlikely to make an employment change unless forced to do so by a lack of flexibility around place of work or hours

- Will be contemplating their exact retirement age and date - an important life-changing phase

The danger of assumptions

Remember that this kind of report provides a guide but should not be used literally. One 28-year-old worker could be married with children and a mortgage, while another is still living at home with no dependents. Would it be right to assume that the first is keen to save for the future while the other is focused on the here and now? Can you assume that all employees over the age of 55 have more disposable cash, or take a greater interest in their benefits package than either of those 28-year-olds?

Understanding your organisation's demographic can help create categories and align employee expectations as a basis, but beyond this life can take unexpected twists: redundancy, grief, illness, trauma, divorce, and addiction. In all of these cases knowing your workforce, and getting crucial input from managers, will help build a fit-for-purpose wellbeing strategy that provides the advice and support they need.

Effective communication

This approach should also enable companies to promote benefits with communications and messaging that resonates with workers. Whether you’re offering a simple Employee Assistance Programme or a royal flush of pensions, salary sacrifice, flexi holidays and recognition schemes, poorly conceived messaging will fail to land well with all workers.

Universal accessibility to all these benefits is also essential if the overall package is fair and equitable for every employee. Some of the best benefits tools are now accessed via smartphone-friendly apps giving 24/7 information in one place: a continuous programme of support, awareness and education for benefits, telling employees what is available, why it’s there, what it can do for them and how they can access it.

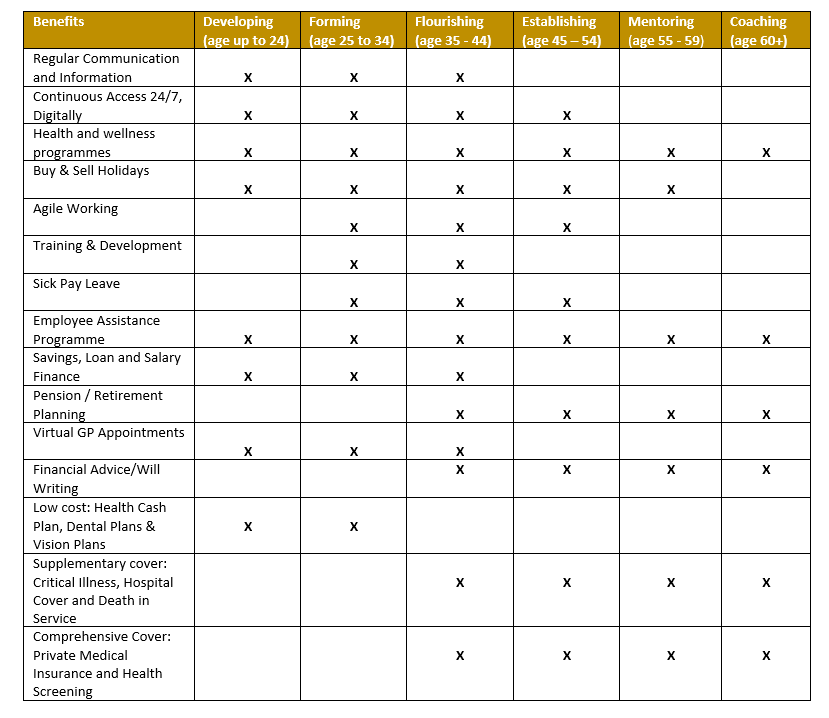

Prevalence of certain benefits by age range– illustration only

Get in touch with Sarah Lardner to discuss how we can help!