Post-Covid, we are experiencing the largest spike in inflation for 30 years, forecast to peak close to 11 percent in the fourth quarter of 2022. Earnings are expected to rise by six percent this year but, with prices settling at a higher level relative to incomes, real household incomes are forecast to fall by 2.5 percent in 2022. More telling still, they will probably remain 7 percent below where they were pre-Covid until 2026 or beyond.

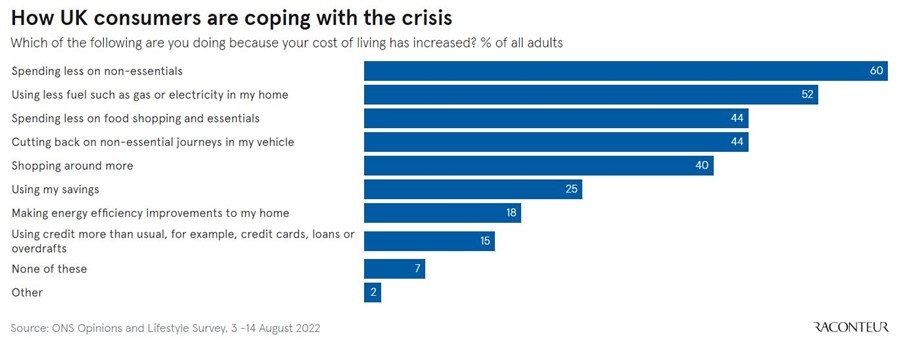

According to the National Institute for Economic and Social Research, "three shocks have combined to shift real incomes onto a permanently lower path. Brexit has raised the cost of imports from continental Europe and incentivised households to switch towards more expensive domestically produced goods and services. The recent rise in energy prices has constituted a large terms-of-trade shock for the UK. Finally, discretionary fiscal tightening over the 2021-24 period, following the shock of Covid-19, has reduced the resources available to the private sector." This graph from Raconteur using ONS data in August 2022 illustrates the measures people are taking.

Employees responding to desperate times

Even with the governmental response, all of this is leaving millions of households across the UK with little to no savings, facing food and energy bills greater than their disposable income. Many will use foodbanks and lean on charities and the desperation will cause thousands to make short-term decisions that will potentially derail careers, leaving jobs for which they have been well trained.

Research by the Homecare Association shows that many care workers are leaving for better-paid jobs at supermarkets or online retailers, who are spotting an opportunity to attract a new workforce, with the vacancy rate in home care reaching 13.5%.

Measuring your response

Companies are taking various measures in response, but those can vary depending on their size and financial robustness. Measures that can be applied to all workers without breaking the bank might include financial education resources and budgeting tools, season ticket loans, childcare vouchers and payroll deductions for savings.

Businesses able to invest a little more might look at paid absence, discounts on insurance and meals or by guaranteeing contractual hours or increasing part-time hours.

At the higher end of the cost matrix, there are inflationary increases to wage, one-off cost of living payments, share purchase plans and increased pension contributions. Accountancy firm PwC announced a 7% uplift in wage for 70% of its UK workforce, with 50% seeing a 9% increase, in line with inflation. Starting salaries across many of its graduate programmes also increased.

Clearly, these kinds of measures are out of reach for many smaller businesses and could end up creating further unforeseen problems if applied.

Playing the long game

So how can companies act to help and retain staff without suffering the pitfalls that may come from quick and reactive measures?

Fix the leak in the bucket - are there efficiencies you have put off but which you could now put into practice, freeing up cash to raise base pay across the board?

Reset the clock on pay review - In terms of pay review and timings, some companies are drawing down against savings or tightening their belt to give staff increases earlier than planned. Is that an option?

Non-monetary reward - Would some staff look beyond pay and instead take extra holiday, food shopping vouchers, tax-free loans, more training or the experience of working in another department or at a higher grade for a limited time?

Salary sacrifice schemes - Are there creative ways you can use salary sacrifice, through pensions, low emission car schemes, cycle to work, or even through the highest-paid working fewer days or taking payment holidays to free up cash to raise base pay lower down the business? Consideration should be made too for those close to the national minimum wage where there is little room for salary sacrifice.

Financial support – raising awareness of financial well-being support can be free, and money management sessions and debt advice can be simple and affordable. Access to financial advisors might be something lower-paid staff would never otherwise consider and for those suffering financial hardship consider offering interest-free loans.

Think flexible - Flexible arrangements enabling staff to save on travel costs could make a huge difference. So could on-site childcare facilities. Some companies also look at salary drawdown schemes to address workers’ cashflow strains.

Think compassionate – In these times offering paid leave for those with caring responsibilities could make a huge difference if affordable. Targeted pay increases, grants or one-off payments for lower-paid staff will support those in need, while also taking into consideration any impact on universal credit.

In these difficult times, it is likely that most companies will need to consider a combination of these measures. The more you understand your workforce the more threads you will give yourself to pull on and the more implications you can anticipate. Strong and thoughtful communication is then key to reinforcing that philosophy and putting in practice an approach that should help retain staff and maintain morale.

More recent Insights by Sarah Lardner:

Diversity in the workplace: why it matters and how you can improve

Pay without Borders – Aligning salary with talent

What can you do to boost employee engagement?